Software companies are not dead

But they are certainly going to evolve

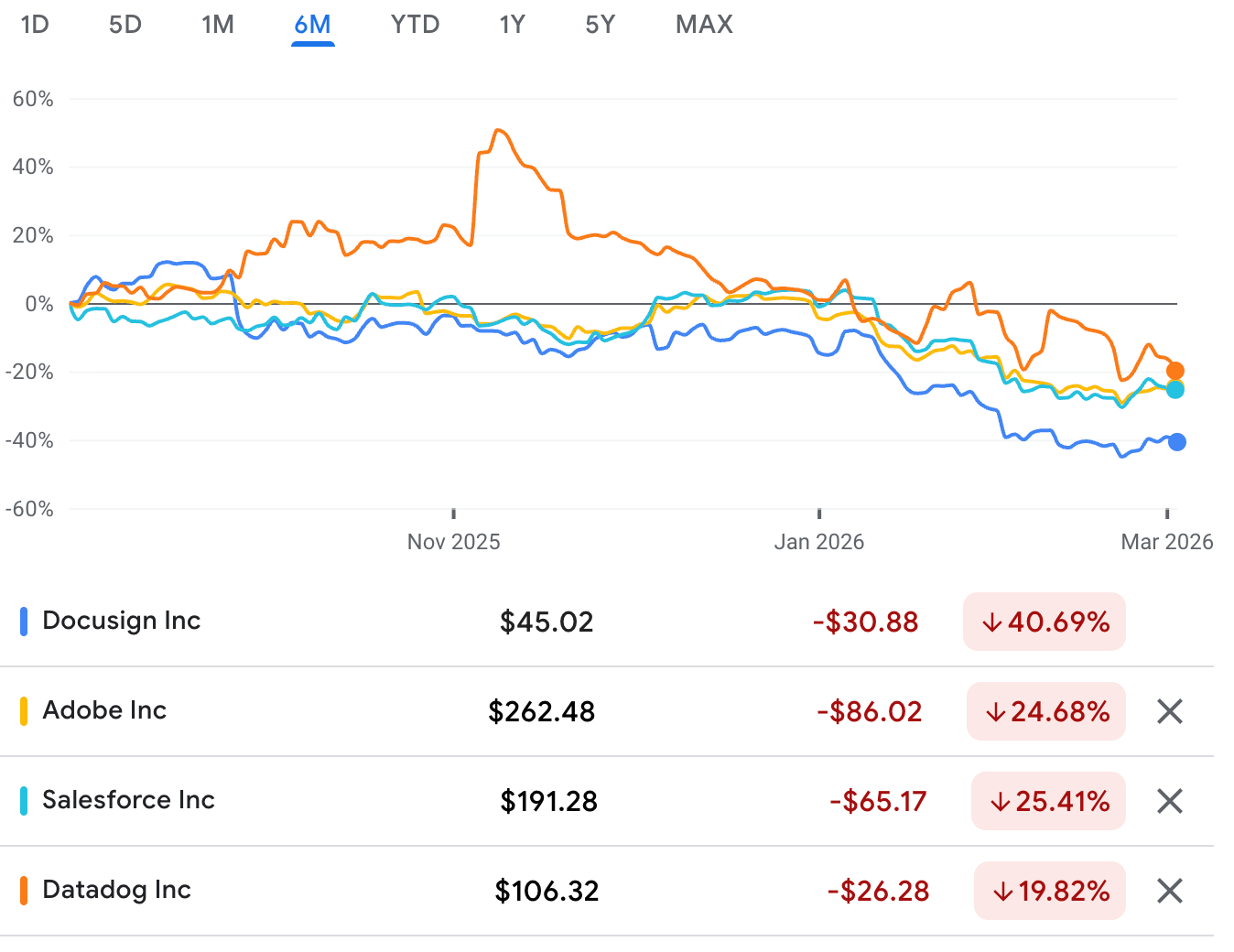

There’s been a lot happening in the last few months. In a not-so-small corner of the equity market, software stocks have taken an AI-induced beating. Here are 4 examples, specifically for SaaS companies:

In each case, there are dual threats:

Investors now believe that customers of these companies might switch to building their own tools with Claude Code, lay off engineers (like we saw Block did this week), cancel SaaS licenses, and rebuild large pieces of their technology services stack in-house

They also believe that the barrier to entry is significantly lower, allowing more AI-native market entrants to put pressure on legacy seat-based pricing

I believe both those fears to be overblown (I’m long this sector). At the same time, the current model of how software is designed, priced and sold will certainly evolve into something new, and this evolution will happen very quickly.

The AI jitters

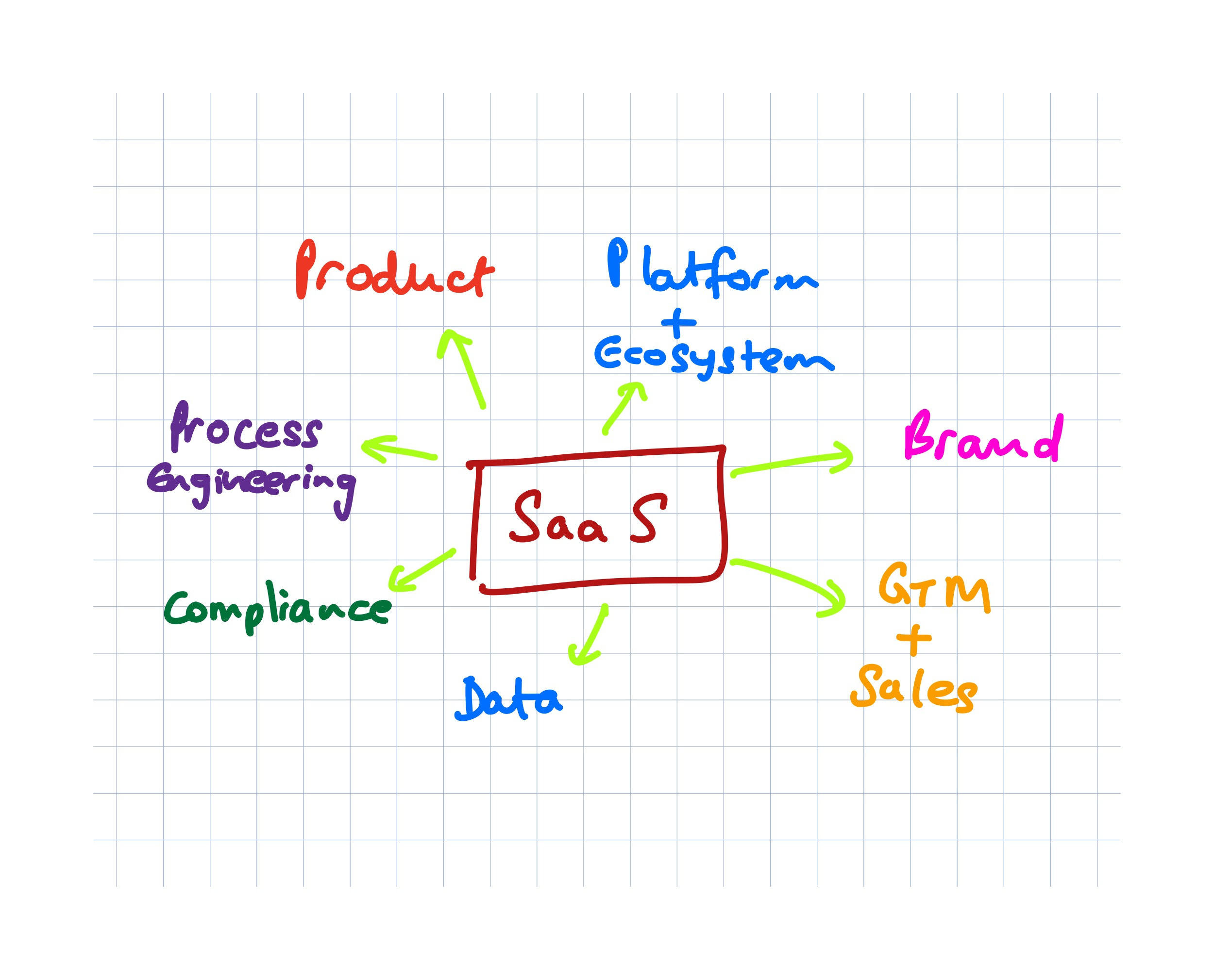

Here’s a simple view of some moats these companies have had, to date:

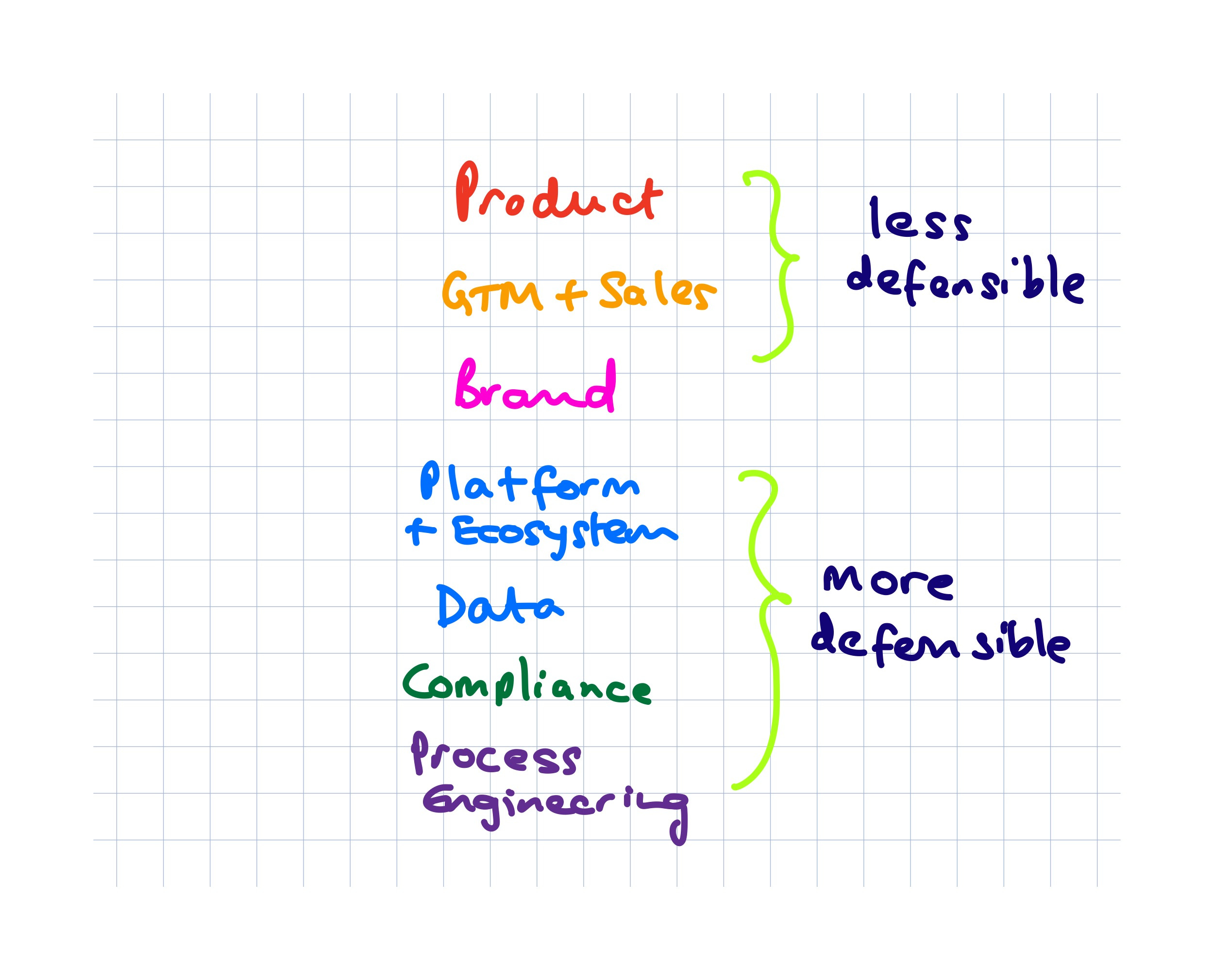

In this sector, the true value of a great company is the sum total of all of these pieces - it’s not just about being able to build a product faster or cheaper, especially to the extent that the barrier to compete has become significantly lower. Here are these pieces again, ranked by defensibility in an AI-powered world:

To summarize, a SaaS company that has deep hooks into an organization’s data, compliance, workflows and processes, and has put in the painstaking effort to build a true platform and ecosystem around its foundational offering, is probably in a better position than a company just relying on its product and sales.

The necessary transitions

There are two key areas that SaaS companies must rapidly evolve to stay relevant and grow:

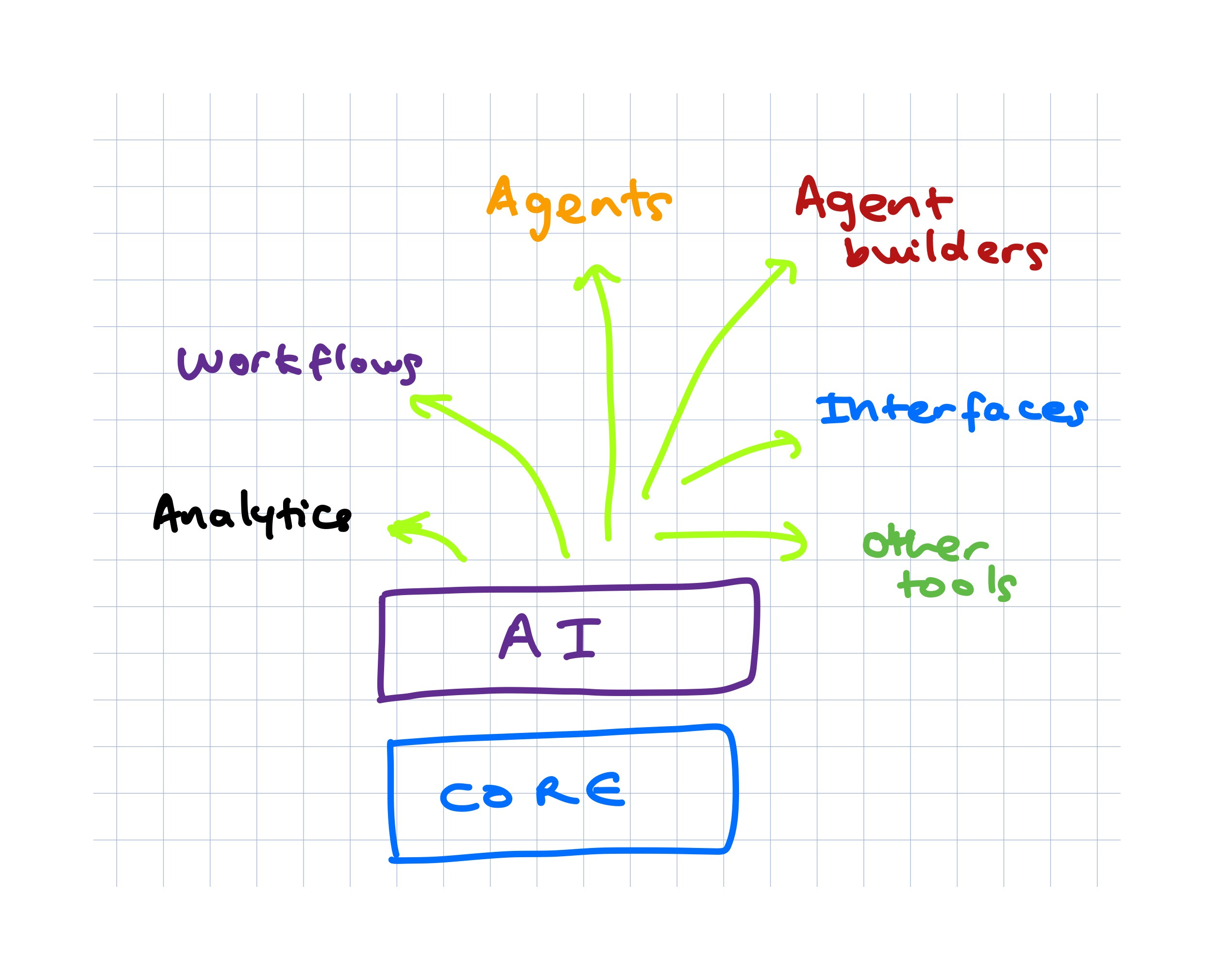

Become a platform

Iterate pricing models

Become a platform

If your only product is an interface that people log into to use, that’s problematic. The key objective should be to offer a foundational offering that offers a solid day-zero experience to any customer, supplemented by a whole bunch of AI features: AI-powered workflows, agents, agent builders, interfaces, and any other AI-powered tools:

We’re already seeing Salesforce do this exceptionally well. They are building enough features around their core offering that reach deep into a client’s workflows that are a moat against anyone - competitors or the client themselves - disrupting their business.

Iterate pricing models

These 4 categories of pricing models cover most of the market:

Historically, seat- or user-based subscriptions have been the go-to pricing models, and are likely most at risk as AI agents start to actively participate in workflows. The price-per-seat isn’t going to easily transition to a price-per-agent.

Instead, I believe we’ll start to see different flavors of usage-based pricing, or pricing that combine a base price for the core offering and usage-based overages for AI tools.

The revenue consequence

The critical point here is that the future revenue and valuation of software companies is much more tightly linked to their adaptability to the new world, and not what their current revenue mix looks like. There are a few reasons for this:

When AI agents are performing work, they’re likely capable of doing more of it than a human could. They operate 24/7, could dynamically resolve issues that previously required human input, and handle much more volume. That translates to much more usage, revenue and stickiness than multiple seats might have provided.

If your revenue is tied to usage, it isn’t bound by the size of a department or by the size of a team.

Usage-based revenue becomes much more durable if you can become the agentic infrastructure layer that brokers all internal workflows at a company.

These point to an expanded ability to grow revenue, but only if SaaS companies are willing to reinvent themselves quickly enough before their existing business is disrupted.

We’ll definitely see some failures, but plenty of successes, and plenty of opportunities for those successes to grow.